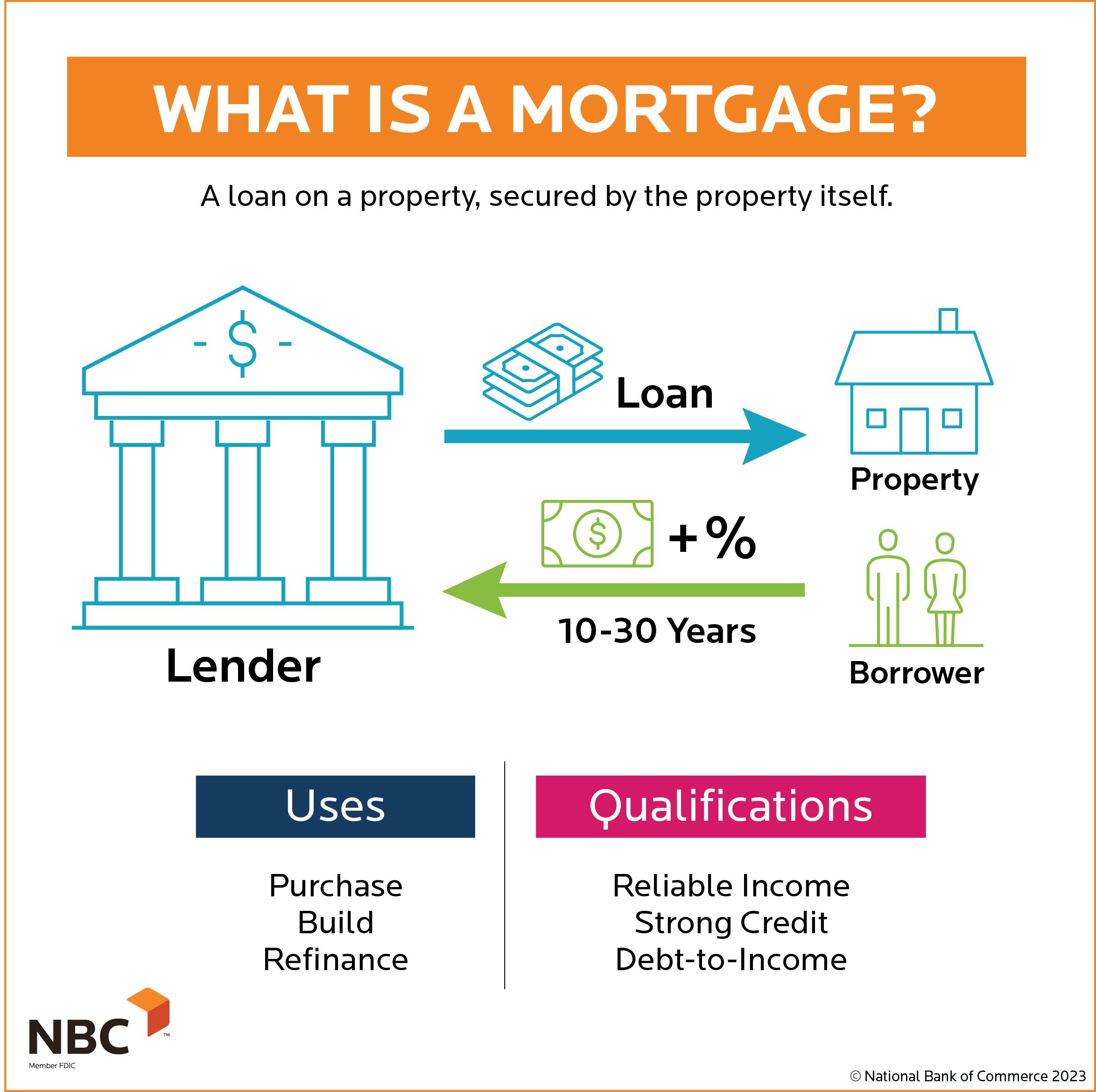

In a world where the ink on your diploma hasn’t even dried but the monthly reminder of your student loan arrives punctually, many might think that owning a home is a chapter reserved for the distant future. However, the American Dream, with its white picket fence, doesn’t have to be deferred indefinitely simply because you carry the weight of educational debt. Whether you’re a recent graduate weighed down by tens of thousands in student loans or a few years into your career still chipping away at that balance, understanding how to navigate the treacherous waters of acquiring a mortgage can make the difference between renting indefinitely and stepping into the home you’ve always wanted. This article sets out to demystify the process, offering critical guidelines and savvy strategies for those aspiring homeowners who are wondering how to balance their student loan obligations with their dreams of purchasing real estate.

Table of Contents

- Understanding Your Debt-to-Income Ratio and Its Impact on Mortgage Approval

- Exploring Loan Options: Which Mortgage Is Right for You?

- Strategies to Improve Your Mortgage Eligibility While Managing Student Debt

- Securing the Best Mortgage Rates with Student Loans: Tips and Tricks

- Concluding Remarks

Understanding Your Debt-to-Income Ratio and Its Impact on Mortgage Approval

Your debt-to-income ratio (DTI) is a crucial financial measurement, particularly when seeking a mortgage. This ratio compares your total monthly debt payments to your gross monthly income, giving lenders an insight into your ability to manage payments and debts effectively. Here’s how your DTI impacts your chances of securing a mortgage loan, especially when you have existing student loans.

Calculating Your DTI: To determine your DTI, add up all your monthly debt obligations—this includes student loans, credit card payments, car loans, and any other debts. Divide this total by your monthly pre-tax income. For instance, if your monthly debts sum up to $2,000 and your gross monthly income is $6,000, your DTI would be approximately 33%.

Lenders typically prefer a DTI ratio of 43% or lower. A lower DTI indicates to lenders that you have a good balance between debt and income, making you less of a risk for default. This is particularly important if you carry additional burdens like student loans. Here’s a comparative look:

| Monthly Income | Student Loan Payment | Other Monthly Debts | Total Monthly Debts | DTI Ratio |

|---|---|---|---|---|

| $5,000 | $300 | $700 | $1,000 | 20% |

| $5,000 | $300 | $1,200 | $1,500 | 30% |

| $5,000 | $300 | $1,700 | $2,000 | 40% |

When it comes to mortgages, keeping your DTI as low as possible is advisable. Here are some strategies to achieve that:

- Increase your income: Consider side gigs or freelance work to boost your monthly income, thereby lowering your DTI.

- Pay down existing debt: Focus on reducing the balance on your credit cards or any higher-interest debts before applying for a mortgage.

- Reconsider your student loan repayment plan: Opt for a repayment plan that lowers your monthly payments, such as an income-driven repayment plan.

It’s important to remember that lenders not only look at the numbers but also at the stability of your income, your employment history, and your credit score. Thus, while your DTI is essential, maintaining a good credit score and a stable job is equally significant.

An often overlooked strategy is to save for a larger down payment. This does not directly lower your DTI, but by reducing the amount of financing needed, it makes your mortgage application more appealing to lenders.

while student loans can indeed impact your DTI and thus influence your mortgage qualification, understanding and managing your DTI can help tilt the scales in your favor. Approach your finances strategically and maintain a holistic perspective to ensure that when you apply for a mortgage, you present yourself as a capable and reliable borrower.

Exploring Loan Options: Which Mortgage Is Right for You?

As you navigate the complexities of acquiring a mortgage while juggling student loans, it’s crucial to understand the different types of mortgages available and identify the one that best fits your financial situation. Below, we explore the most common mortgage options to help you make an informed decision.

Fixed-Rate Mortgages offer the security of a consistent interest rate and monthly payment for the entire loan term. This predictability makes it easier to budget, especially important when you are balancing student loan obligations. Choosing a fixed-rate mortgage can shield you from fluctuations in interest rates, ensuring stability.

Adjustable-Rate Mortgages (ARMs), on the other hand, begin with a lower interest rate that may increase or decrease with market trends after the initial fixed period. This option might be suitable if you anticipate a rise in your income or plan to pay off your mortgage quickly.

Government-Insured Loans such as FHA, VA, and USDA loans provide opportunities for those with less savings for down payments or not perfect credit scores. These programs often come with specific requirements but can offer smaller down payments and have flexible credit requirements, which might be beneficial for those still handling student debt.

Conventional Loans are typically suited for borrowers with strong credit, stable employment history, and at least a 20% down payment. If you meet these criteria, a conventional loan might offer lower interest rates and PMI (private mortgage insurance) that can be dropped once you achieve 20% equity in your home.

| Type of Loan | Initial Down Payment | Credit Score Needs | Suitable for |

|---|---|---|---|

| Fixed-Rate Mortgage | 5-20% | 620+ | Budget stability seekers |

| Adjustable-Rate Mortgage | 5-20% | 620+ | Short-term homeowners |

| FHA Loan | 3.5% | 580+ | Low down payment buyers |

| VA Loan | 0% | 620+ | Veterans |

| USDA Loan | 0% | 640+ | Rural homebuyers |

| Conventional Loan | 20% | 620+ | Financially established |

Your choice of loan might also depend on the area where you wish to buy a property. For instance, USDA loans are specific to rural areas, whereas other loans can be used in various geographic locations. Assessing the location alongside your financial capacity and homeownership goals is crucial in making your decision.

Moreover, consider the future impact of your student loans on your ability to qualify for and manage a mortgage. Balancing both financial responsibilities requires foresight and planning. Drafting out a detailed budget including your potential mortgage and existing student loan payments can prevent future financial strain.

Understanding your DTI (Debt-to-Income) ratio is also imperative. Mortgage lenders use this ratio to determine your eligibility. Keeping your DTI within acceptable limits while managing student loans is a balancing act that demands careful scrutiny of your finances.

Strategies to Improve Your Mortgage Eligibility While Managing Student Debt

While juggling student debt, the prospect of buying a home may seem daunting. However, with the right approach, you can improve your mortgage eligibility. Here are some effective strategies to consider.

Understand Your Debt-To-Income Ratio

Your debt-to-income (DTI) ratio is crucial in the mortgage process. Lenders use this figure to assess your ability to manage monthly payments and repay debts. Strive to lower your DTI by increasing your income, paying down your student loans, and avoiding new debt.

Enhance Your Credit Score

A higher credit score can significantly boost your mortgage prospects. Ensure you make student loan payments on time, reduce your credit card balances, and avoid opening new credit accounts excessively. Periodically review your credit report for any errors and dispute them if necessary.

Explore Different Mortgage Programs

Some mortgage programs are more forgiving regarding student debt. For instance, FHA loans generally have more lenient guidelines on debt ratios and credit scores. Meanwhile, Fannie Mae offers options that can consider income-based repayment plans when calculating your DTI.

| Program | Feature |

|---|---|

| FHA Loans | Lower down payment and flexible credit requirements. |

| Fannie Mae | Student loan cash-out refinance options. |

| VA Loans | No down payment required and no PMI. |

Consider a Joint Application

If you have a partner with a better financial standing, applying together might be beneficial. A joint application can help balance out your DTI and reinforce your loan application’s credibility. However, this should be considered carefully, as it also implies shared financial responsibility for the mortgage.

Consolidate or Refinance Student Loans

If your student loans have a significantly high interest rate, consider refinancing or consolidating them into a single loan. This could reduce your monthly payments and your DTI, making room for a mortgage. Just be cautious about switching federal student loans to private, as it could mean losing certain benefits.

Save for a Higher Down Payment

Increasing your down payment can make a substantial difference. It not only lowers your mortgage’s principal but may also give you more favorable interest rates and reduce the need for private mortgage insurance (PMI). Start a dedicated savings plan specifically for this purpose.

- Automate savings to ensure consistent contributions.

- Explore high-yield savings accounts or certificates of deposit for better returns on your savings.

Stay Prepared for Lender Scrutiny

When you apply for a mortgage with student debt, expect lenders to scrutinize your financial situation more closely. Being prepared can make the process smoother and less stressful. Compile all relevant financial documents in advance and be ready to explain any discrepancies in your financial history.

While balancing student loans with the pursuit of homeownership is challenging, it’s entirely achievable with careful planning and strategic action. Take these steps seriously, and you could soon find yourself holding the keys to your new home.

Securing the Best Mortgage Rates with Student Loans: Tips and Tricks

Navigating the world of mortgages with student loans hanging over your head can seem daunting, but with the right strategies, securing an affordable home loan is entirely achievable. Here, we’ve compiled essential tips and tricks that can help you make savvy decisions about your mortgage application and improve your chances of getting favorable rates.

Improve Your Credit Score: First and foremost, a healthy credit score is crucial. Although student loans can impact your score, timely payments can actually boost it. Ensure all your debts are managed properly. Regularly check your credit reports for any errors or inconsistencies and rectify them immediately.

Maintain a Stable Employment Record: Lenders favor applicants with stable, predictable income. A steady job not only reflects your ability to manage ongoing loan payments but also positions you as a lower-risk borrower. Consider holding off on any career changes until after your mortgage is approved.

Consider a Longer Loan Term: Opting for a 30-year mortgage over a shorter loan term can decrease your monthly payments, making them more manageable in conjunction with your student loan obligations. This, however, will result in more interest paid over the life of the loan, so it’s a balance of immediate affordability vs. long-term cost.

Here’s a simple comparison to help you understand the potential difference:

| Loan Term | Monthly Payment | Total Interest Paid |

|---|---|---|

| 15 years | $1,600 | $89,000 |

| 30 years | $1,200 | $176,000 |

Save for a Larger Down Payment: The more you put down upfront, the less you need to finance, which could lead to better interest rates and lower monthly payments. This is particularly beneficial for those with student loans as it demonstrates financial responsibility to lenders.

Lower Your Debt-to-Income Ratio (DTI): Before applying for a mortgage, focus on reducing your debt-to-income ratio. This figure measures your total monthly debt against your income. Lenders typically look for a DTI of 36% or lower, including your future mortgage payment. Strategies include paying down debt aggressively or increasing your income by taking on freelance gigs or a part-time job.

Explore Mortgage Programs: Look into government-backed mortgages such as FHA, VA, or USDA loans, which may be more forgiving of student loan debt and often require lower down payments. Additionally, some states offer special programs for first-time homebuyers that can also accommodate those with student loans.

Consult with a Mortgage Broker: A seasoned mortgage broker can provide invaluable advice tailored to your specific financial situation. They can help you understand the array of mortgage products available and decide which option best suits your needs while taking into account your student loan obligations.

By keeping these strategies in mind and preparing accordingly, you can bolster your mortgage application and secure a rate that fits comfortably within your budget, notwithstanding student loans. Remember, patience and careful planning are your best tools when undertaking this significant financial step.

Concluding Remarks

As we reach the close of our deep dive into navigating the waters of mortgages with student loans, it’s clear the journey to homeownership, though dotted with various financial considerations, is not an insurmountable voyage. The key lies in careful preparation, informed decision-making, and tenacity. Whether you’re balancing hefty student loans or just beginning to untangle your financial threads, the dream of slipping your key into the door of your own home need not be deferred. Equip yourself with these guidelines, seek advice tailored to your unique financial landscape, and step forward with confidence. May your path lead you to the welcoming threshold of a home that not only shelters your dreams but also bears witness to the realization of them.