In the grand tapestry of investment opportunities, buy-to-let properties loom vibrant and enticing, offering the twin allure of rental income and potential capital growth. But before you can open the door to becoming a landlord, there’s a critical key you’ll need to turn: securing a buy-to-let mortgage. This article will serve as your comprehensive guide to navigating the often complex waters of property investment financing, illuminating the path from curious onlooker to confident property owner with foresight and expertise. Whether you’re dreaming of a quaint urban flat buzzing with the energy of city life or a serene suburban home that’s a commuter’s retreat, understanding buy-to-let mortgages can help turn your real estate aspirations into tangible assets. So, buckle up and prepare for a deep dive into the world of property investment, where we decode terms, unravel requirements, and clear the fog around the financial frameworks that empower today’s investors to build tomorrow’s fortunes.

Table of Contents

- Understanding Buy-to-Let Mortgages: An Overview

- Eligibility and Requirements for Prospective Landlords

- Exploring the Financial Implications: Costs and Returns

- Navigating Legalities and Regulations in Buy-to-Let Investing

- Final Thoughts

Understanding Buy-to-Let Mortgages: An Overview

Buy-to-let mortgages are a fascinating financial tool designed for purchasing property intended to be rented out. Unlike traditional mortgages, where the borrower plans to reside in the purchased property, buy-to-let mortgages are commercial investments. They enable borrowers to manage a property portfolio, potentially earning a profit both through rental income and property value appreciation.

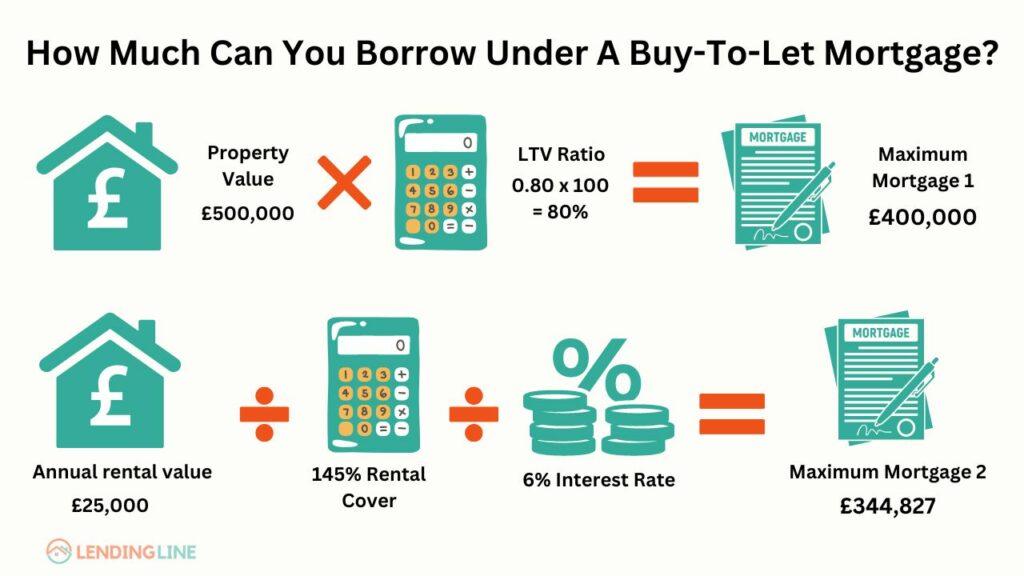

One of the primary considerations in obtaining a buy-to-let mortgage is the expected rental income. Lenders typically require that the rental income exceed the mortgage payments by a certain percentage, ensuring the property can self-sustain even in fluctuating market conditions. Rental coverage ratio, often set at around 125%-145%, acts as a buffer protecting both the investor and the lender.

Eligibility criteria for these mortgages are distinct from personal home loans. Lenders evaluate potential borrowers based on:

- Age – Most banks will require you to be at least 25 years old.

- Income - Some lenders might demand a minimum annual income, aside from rental predictions.

- Investment experience - Familiarity with property investments may be advantageous.

- Credit history – A solid credit history reassures lenders of your risk management skills.

Lenders also place a cap on the maximum amount they will loan, typically determined as a percentage of the property’s value, known as the loan-to-value ratio (LTV). Most buy-to-let mortgages have an LTV limit around 75% to 85%.

Additionally, the interest rates on buy-to-let mortgages can be higher compared to standard mortgages. They also frequently come in the form of interest-only loans, meaning monthly payments only cover the interest. This can be financially manageable for landlords as the principal will be covered through the eventual sale of the property, though it requires significant market analysis and foresight.

| Feature | Detail |

|---|---|

| Interest Type | Often interest-only |

| Typical LTV | 75% – 85% |

| Rental Coverage Ratio | 125% - 145% |

| Loan Term | 15 to 25 years |

Mortgage fees also form a significant part of the buy-to-let puzzle. Prospective landlords should expect to encounter arrangement fees, valuation fees, and potentially higher conveyancing costs compared to residential mortgages. Though initially steep, these fees are often rolled into the loan, spreading the cost over the loan’s lifetime.

Understanding the nuances of buy-to-let mortgages can empower you as an investor. With prudent management and strategic planning, leveraging these financial instruments can transform a simple property investment into a robust income-generating venture. Always ensure thorough homework and possibly consultation with financial experts to align such investments with your long-term financial goals.

Eligibility and Requirements for Prospective Landlords

Stepping into the world of property investment with a buy-to-let mortgage is an exciting venture, but it does come with its set of prerequisites. Prospective landlords must meet certain eligibility criteria and fulfill specific requirements to ensure they are prepared for the responsibilities of managing rental property. Here’s what you need to know:

Age and Residency: Most lenders require borrowers to be at least 21 years old, but the ideal age bracket may vary depending on the financial institution. Additionally, you generally need to be a resident in the country where the property is located, although some lenders might approve non-resident landlords under stringent conditions.

Income Stability: A stable income is crucial, not just from your rent yields but from other sources too. Lenders typically look for individuals with annual incomes over a certain threshold outside of the rental income to cover mortgage payments during void periods (when the property is unoccupied). Employment history and job security can also be evaluated.

Credit Score: A good credit score reassures lenders of your financial reliability and creditworthiness. Potential landlords should ensure their credit history is clear of any significant issues like defaults or CCJs (County Court Judgments).

Existing Property Ownership: Some lenders might be more willing to grant a buy-to-let mortgage to individuals who already own property, either outright or with an ongoing mortgage. This shows experience in handling property-related financial commitments.

- Deposit Requirements: Typically, a higher deposit is required for buy-to-let properties compared to standard residential mortgages. Expect to need at least 25% of the property’s value, though some lenders might require more.

- Rental Income: Lenders will usually require that the expected rental income be 25-30% higher than your mortgage payment, a measure to ensure you can cover the loan even if rental prices fall.

- Professional Advice: Engaging with a financial advisor or a mortgage broker experienced in buy-to-let properties can provide invaluable insights and aid with the complex application process.

Moreover, understanding the legal responsibilities as a landlord is essential. This includes ensuring the safety of your property, getting the necessary landlord licenses, and adhering to local housing laws. Regular property maintenance and management must also be planned to avoid any future legal complications.

The table below showcases the basic financial requirements and ratios often considered by lenders:

| Requirement | Description | Typical Values |

|---|---|---|

| Deposit | Percentage of property’s value | 25%-40% |

| Rental Coverage Ratio | Rental income vs. mortgage payment | 125%-130% |

| Minimum Income | Outside of rent income | Varies, often around $25,000 |

Each lender’s criteria can vary significantly, and the market’s state or specific property issues like its location and condition can also influence eligibility. By preparing all the necessary documents and understanding these requirements, you can streamline the application process and increase your chances of success.

Exploring the Financial Implications: Costs and Returns

When venturing into the realm of buy-to-let mortgages, understanding the fiscal terrain is vital. This means singularly examining both the costs you will incur and the potential returns. A prudent investor not only scrutinizes the immediate expenses but also the long-term viability and profitability of their investment.

Initially, the primary cost involves the deposit. Typically, this spans from 20% to 25% of the property’s purchase price, significantly higher than those required for standard residential mortgages. This larger up-front investment impacts your immediate financial flexibility but is essential for securing a buy-to-let mortgage.

Apart from the deposit, there are running costs that must be managed. These include:

- Mortgage repayments – Variable depending on the interest rate and loan amount.

- Property maintenance – Regular repairs and maintenance to keep the property in good condition.

- Management fees – If you hire a property manager to handle daily operations.

- Insurance – Building insurance and possibly landlord insurance to cover potential damages and liabilities.

Beyond these expenditures, you should be aware of the stamp duty levy applicable on additional properties, which adds a significant percentage to the cost depending on the property value. Planning for these taxes in advance avoids unexpected financial strain.

Now, shifting focus to the returns on your investment:

| Rental Yield | This is your annual rental income as a percentage of the property purchase price. |

|---|---|

| Capital Growth | Over time, the property value may increase, yielding potential profits during resale. |

| Tax Benefits | Some expenses related to letting out the property can be deducted for tax purposes, thus reducing the tax burden. |

Calculating rental yield is straightforward but crucial. An appealing yield generally falls between 5% and 8%. However, this can vary widely based on location, property type, and market conditions. Therefore, understanding market dynamics plays a pivotal role in predicting successful returns.

Regarding capital growth, historical data in certain areas may suggest robust growth, while in others, it could predict stagnation or even a decline. Keeping an eye on future developments, economic policies, and changes in demographics can provide insights into potential value changes.

To encapsulate, diving into the buy-to-let mortgage landscape demands a broad appraisal of both the overt and covert expenditures and anticipated income. A balanced perspective will not only safeguard against unforeseen financial setbacks but also pave the path towards a fruitful real estate investment venture.

Navigating Legalities and Regulations in Buy-to-Let Investing

Embarking on the buy-to-let journey involves more than just purchasing property; it requires a deep understanding of the legal and regulatory framework surrounding rental investments. In this section, we delve into the labyrinth of compliance ensuring that your venture remains legitimate and profitable.

Initially, the most pivotal legality to confront is securing a buy-to-let mortgage. Unlike standard residential mortgages, buy-to-let mortgages are designed specifically for properties that will be rented out. Lenders assess these loans differently, focusing primarily on the potential rental income rather than the borrower’s personal income. Here’s a quick rundown:

- Loan-to-Value (LTV) ratios for buy-to-let mortgages generally hover around 75-85%, meaning you’ll need a sizeable deposit up front.

- Interest rates on these mortgages might be slightly higher to offset the perceived risk lenders undertake.

- Affordability tests ensure that the expected rental income surpasses the mortgage payments by a certain percentage, commonly 125-145%.

Next, understanding the array of property laws is crucial. Landlord obligations include securing the property’s safety for tenants, adhering to fire safety regulations, and ensuring all necessary inspections are up-to-date.

Additionally, familiarity with the Tenancy Agreement legalities remains paramount. This written agreement is fundamental and outlines both the landlord’s and tenant’s rights and responsibilities. Ensure it comprehensively covers scenarios like rent payments, deposits, property maintenance, and guidelines for dispute resolution.

| Key Regulation | Impact |

|---|---|

| Gas Safety Certification | Annual check required by law to ensure all gas appliances are safe. |

| Energy Performance Certificates (EPC) | Properties must have an EPC rating of ‘E’ or above to be rented out. |

Investors must be vigilant about the financial aspects, specifically the tax implications. Rental income is taxable, and landlords must account for this in their annual self-assessment tax returns. Changes to tax relief rules on mortgage interest have altered the profitability calculations for many investors, making professional financial advice invaluable.

For international investors, additional hurdles such as unfamiliarity with local laws, potential double taxation, and more convoluted procurement processes can complicate things. Working with a local solicitor and tax advisor can streamline the process, ensuring compliance with local regulations and optimizing tax strategies.

It’s also wise to keep abreast of ongoing regulatory changes in the housing market. Local authorities may impose more stringent regulations on rental properties, such as licensing schemes for landlords or caps on rent increases. Being proactive and informed can significantly mitigate legal risks and enhance the success of your investment.

the complexity of legalities and regulations in buy-to-let investing should not discourage investors but should prompt a thorough approach to education and compliance to safeguard and capitalize on their investments.

Final Thoughts

As we come to the close of our journey through the intricate web of buy-to-let mortgages, it’s clear that stepping into the realm of property investment is both an exciting and demanding endeavor. We’ve unpacked the essentials, navigated through the nuances, and illuminated the path that could lead you to become a potential landlord. Whether stirred by stories of rental yields or steered by the ambition to expand a budding portfolio, you now hold the foundational knowledge to bridge the gap between contemplating and actualizing your property investment aspirations.

Remember, each property tells a story, and each investment carries its unique blueprint of challenges and rewards. As you close this guide and potentially open the doors to new properties, keep in mind that the world of real estate investment requires not just financial acumen, but also a keen sense of timing, an understanding of local market trends, and an unwavering patience. Here’s to building futures, one property at a time. Dive in but tread wisely, and may your buy-to-let ventures prosper!